Understanding how your credit is calculated is the first step to clearing up your credit history and improving your credit scores. The FICO scoring system takes several key aspects of your credit file in order to come up with the number that the creditors use.

Because all three bureaus have their own relationships with creditors who report your financial history, it is quite likely that your credit score will vary among Equifax, Experian, and TransUnion.

This also means that any inaccurate information that is on one report may or may not be on the other two. That’s why some lenders may approve you for a loan when they pull your credit report versus another lender who denies you elsewhere — they could be using different information pertaining to your credit history.

It’s important to check all three of your credit reports regularly so you know exactly what items are potentially damaging your credit score.

Once you have the facts, you can develop a plan to get your finances back on track. And since the information listed on each credit report can differ, you should always comb through all three to get your full credit picture.

We’ll show you how to clean up your credit so you can increase your FICO score and start getting better access to credit cards, loans, mortgages, and other types of financing you may need.

What Items Can Damage Your Credit Score?

There are three areas where your credit scores may be impacted, outside of major negatives such as bankruptcies, foreclosures, and judgments. These common damaging items include:

- Delinquencies

- Collection Accounts

- Charge Off Accounts

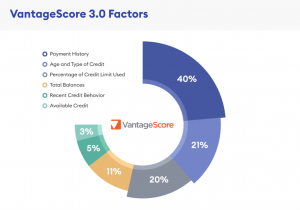

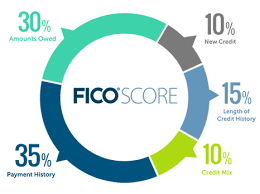

As you can see by the charts below, there is wide room for improvement by getting inaccurate and damaging information off of your credit score, and the sooner, the better:

Chart – I

Chart – II

How to Start Cleaning Up Your Credit

Each type of negative item comes with different nuances for getting them removed from your credit report. But before you even start that process, you have to prepare your case effectively.

Follow these steps to get started so that you can successfully clear your credit regardless of the type of items causing damage. Thorough preparation is the best way to set yourself up for a quick dispute process that is free of headaches.

Order & Review your Three Credit Reports

You’re entitled to free copies of your credit reports from Equifax, Experian, and TransUnion each and every year. You can’t dispute anything until you know what’s on there, so this is the absolute first step to cleaning up your credit. Go through each section and look for any potential red flags, including:

- Inaccurate personal information, such as your name or social security number

- Accounts that don’t actually belong to you

- Inaccurate account details, such as amounts owed or credit limits

- Missing information, such as closed accounts being listed as open

- Outdated information, such as negative items still listed after the seven- or ten-year limit

Determine Which Mistakes to Dispute and Gather Evidence

Any mistake can be disputed, especially if it’s hurting your credit score. Go through each of your credit reports and mark which ones you want to challenge.

If you have a lot, you might want to narrow things down in one of two ways. The first method is to only dispute a few at a time; if you choose to do this, start with the most damaging items so you can get them quickly removed from your report.

The second method is to contact a reputable credit repair company like Sky Blue Credit Repair and have them help you with your dispute process, which can be especially beneficial if you feel overwhelmed or unsure of the process.

Once you decide which items to dispute and whether you’re going to do it on your own or get a professional to help you, you need to gather all of the evidence to support your case. You don’t need to include it in your dispute request because the burden of proof remains with the credit bureau.

It’s their job to verify each negative item with the relevant creditor, and if they can’t do that, then the item must be removed. But if the creditor supplies faulty information, it’s smart to have your own paperwork on hand to support your case.

Keep these documents ready to have when you need them. When working with a credit repair company, they might also request this information from you to bolster your case during their own dispute process.

How do I clear my credit of delinquencies?

If you’ve been 30 days or more past-due with your bills, you may find delinquencies listed on your credit report. While these delinquencies are definitely damaging, they can sometimes be easy to fix.

Start with the late payments that are the most past-due, i.e. the 90-day and 120-day debts. The reason to start here is because these are the accounts that are most damaging to your credit scores, and they are also the accounts that are most likely to be sent to collections or charged off.

If you can make a payment that will bring you current, you should call your creditor and be prepared to negotiate. If these delinquencies are for an account that is currently open, you have some leeway here.

Ask the creditor if they are willing to re-age the account (it works to your benefit if the account is still open and you want to keep it). This will effectively let them update the account as being paid on time, rather than showing a history of past-due payments.

For the 30-day and 60-day accounts, if you have any paperwork that shows you made or mailed the payment within that 30-day window, you should call up the creditor and dispute the derogatory listing.

Many times, creditors are willing to work with a good customer who is only rarely late with payments. Otherwise, you will have to make your complaint in writing with the credit bureau and your creditor in order to get the inaccurate information updated.

How do I clear my credit of charge offs?

Debt that has been charged off means that the creditor has declared it unlikely that you’ll ever repay the debt. They still have the right to attempt to collect the money that is owed.

However, in most instances, they’ll sell it for pennies on the dollar to a collection agency to begin their own collection process. When it comes to your credit score, charged off debt has a greater negative impact than late payments.

Creditors don’t like to see debts that haven’t been repaid and are much less likely to extend credit to you while charge offs are on your report because it essentially looks like abandoned debt.

Some loans, such as mortgages, require that all charged-off debt be settled or paid off before you can qualify, no matter what your credit score happens to be. Getting your credit clear of a charge off will take more work, but it is possible.

You will need to:

- Contact the creditor and ask if they are willing to settle – this can be done by phone or by letter, but the most effective way to have proof of the settlement is to get everything in writing.

- Make the payment in certified funds – so you have proof the debt is paid.

- File a dispute with the credit reporting agency and use your proof of payment to support having the disputed charge-off removed.

Sometimes you’ll luck out, and a creditor that has been paid won’t bother to respond to the dispute because they have payment in hand. This will get the item deleted from your report entirely.

Other times, the creditor will update your account to say ‘Settled,’ which is still better than having an unsettled charge-off on your credit report. However, it won’t help your scores as much as a deletion would.

How do I clear my credit of collections?

Collection accounts are usually the most complicated issue on anyone’s credit report. These are the collection accounts that have been sold to debt collection agencies – sometimes multiple times.

The collection agencies have zero interest in helping you. They only care about being paid as much as possible. However, there are some bright spots when it comes to getting your credit clear of collections:

- If the debt is past the reporting limit (generally more than 7 years old) then the collection agency cannot list it, and you can dispute the information to have it removed.

- If the collection agency has reported the wrong date, the wrong amount, or other erroneous information, you can dispute that as well and have the negative listing deleted.

- You have 30 days to request validation from the time the creditor first contacts you. In this time, they cannot perform any collection activities and they cannot add the debt to your credit report while the investigation is ongoing.

For older debts especially, collection agencies are often unable to come up with accurate information that proves they own the debt and that you owe it – so more often than not, it pays to dispute any inaccurate information.

Understanding these basics to clear up your credit will put you on the right path, but it’s only the first step. The sooner you get actually get started repairing your credit, the better off you’ll be, both financially and emotionally in the future.

What to Do After the Dispute Process

Once your dispute is removed, there are a couple of steps you can take to continue clearing up your credit.

First, ask the credit bureau to send notification of the change to any financial institution that has accessed your credit report in the last six months. They can do the same for any potential employer that has viewed your credit report over the last two years.

Just note that these actions don’t happen automatically, you have to make the request in writing to each applicable credit bureau. But it’s a worthwhile trick to implement if you’ve been trying to get credit recently or if you’ve been applying for a new job requiring a credit check.

In the event your request for a removal is denied, there are a few more methods to try. First, you can always wait for the negative item to drop off naturally.

Most stay on your credit report for seven years and actually stop hurting your credit score after the first few years lapse. If you’re close to that drop-off mark, it may be worth just exercising a little patience.

If you’ve tried to clear up your credit on your own, consider hiring a professional. Depending on how much your bad credit is costing you in high interest rates or lack of credit altogether, the fee for a professional credit repair company could likely be worth it.

A final option is to ask the credit bureau to include your own note on your credit report. This allows you to provide a brief description of your side of the story so that future creditors reviewing your report can consider any additional details you wish to include.

How can you clean up your credit report fast?

The credit repair process certainly takes some time. But once you’ve initiated the dispute process on your inaccurate negative items, there are other things you can do to clean up your report quickly.

One way is to reduce or eliminate your revolving debt, particularly from high-interest credit cards. Pay down high balances as quickly as possible and your credit score will benefit from this lower debt utilization.

You could also consider a debt consolidation loan, which transfers your credit card debt to a fixed installment loan. You could save money on your interest rate, and also improve your credit by switching your revolving debt to an installment loan. Your credit mix accounts for 10% of your score; while not huge, every bit helps, especially when looking for short-term solutions.

Source: Lauren Ward [https://www.crediful.com]